Gail, a 52-year-old real estate entrepreneur, felt like she was drowning. Despite generating substantial income from her business, she felt overwhelmed by mounting expenses. Her journey from immigrant to successful realtor had taught her to work hard, but not how to make her money work for her.

She had cash flowing in, but it immediately flowed out to business expenses, family needs, and regrettable purchases.

Gail's breakthrough moment came when family fights about money reached a breaking point. She realized that all her hard work building a successful real estate business meant nothing if she couldn't secure her family's financial future. At 52, retirement was approaching fast, and she had no clear plan beyond hoping her properties would somehow provide passive income.

"Keeping up with personal, business, and emergency expenses was a problem,” Gail said. “It always gave me headaches. But when I finally got some help from Doing Well, it really changed things for us."

Intro: Understanding high-earning overwhelmGail shared her situation as a real estate entrepreneur drowning in expenses despite her high income. Her Doing Well coach understood the specific challenges of managing business and personal finances simultaneously, plus the stress of approaching retirement without a clear plan. This was her space to address fears about property investments and the pressure of providing for family while securing her own future.

Categorize: Making sense of complex finances

Together, they reviewed all her accounts: business income, personal expenses, multiple property payments, and investment losses. They identified how her business expenses were eating into potential retirement savings, uncovering spending patterns and property purchases that weren't aligned with her retirement goals.

Budget: Creating entrepreneur-friendly systems

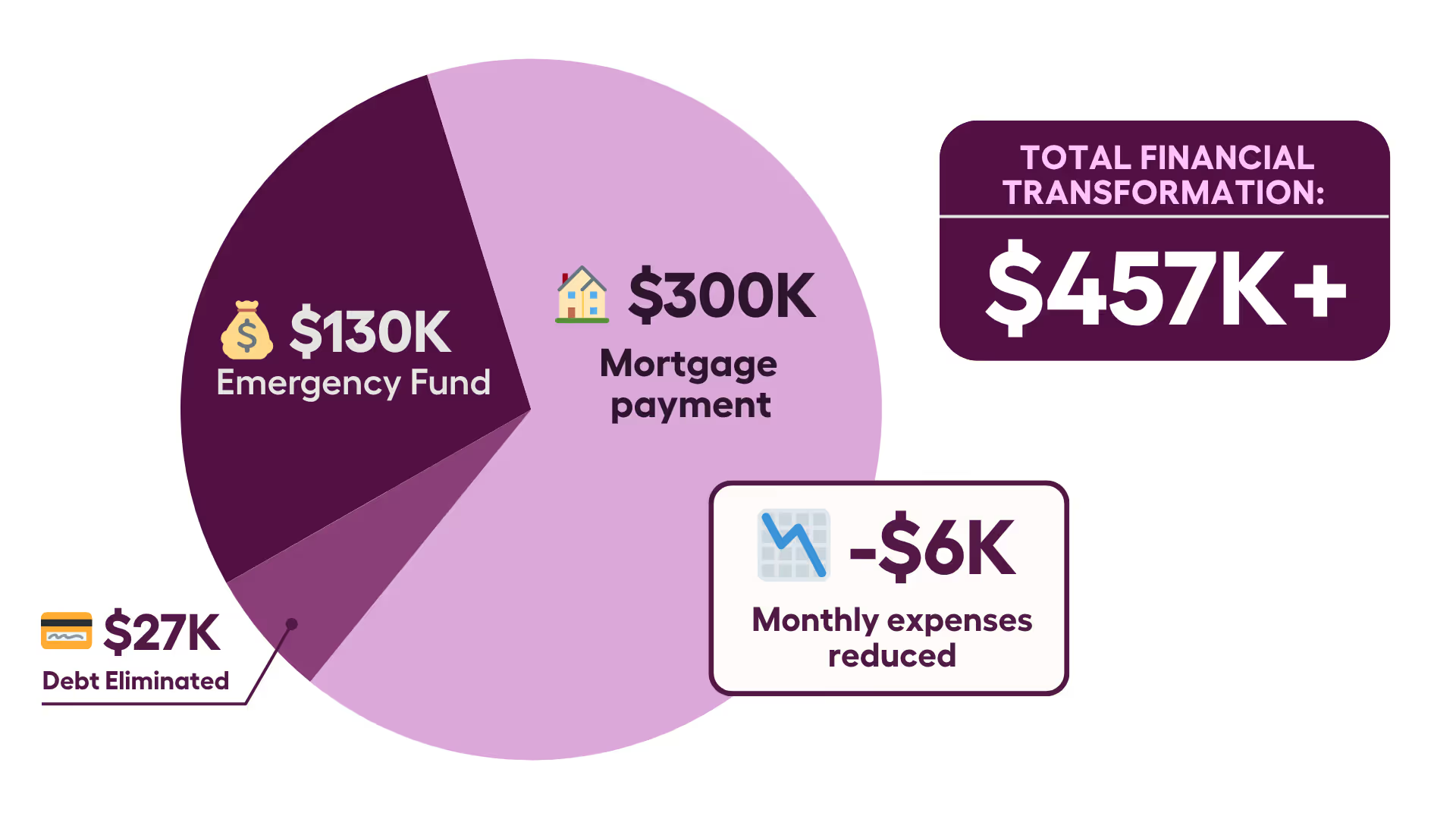

They created a sustainable budget that separated business and personal finances while accommodating her generous personality. Gail reduced her monthly personal and business expenses by $6K and canceled unused subscriptions, creating clarity between necessary business investments and personal lifestyle choices.

Plan: Building her retirement foundation

Gail's comprehensive debt elimination plan addressed her immediate needs: $27K car loan completely paid off, 3 credit cards paid off and closed, and $300K applied toward her mortgage. Most importantly, she allocated $130K into an emergency fund (something she'd never been able to establish due to ongoing property and car payments).

Check-in: Staying on track through business fluctuations

Regular check-ins helped Gail navigate her business resurgence while staying committed to her retirement preparation goals. She successfully sold properties to improve her financial standing and established systems that could weather the ups and downs of real estate income while building toward her dream of multiple rental properties.

Instead of generic budgeting advice, Gail got a custom system designed around her complex real estate business, family responsibilities, and retirement timeline for building passive rental income.

Doing Well designed a systematic debt payoff strategy for Gail. That means prioritizing high-interest debt, strategically selling properties, and automating payments that aligned with her business cash flow cycles.

Understanding Gail's generous nature and tendency toward impulsive purchases, Doing Well focused on creating abundance through strategic property investments and systematic wealth building rather than emotional spending.

Since Gail joined Doing Well, financial stress no longer dominates her family’s conversations. Now she's able to look forward: planning strategic property acquisitions, building passive income streams, and creating the retirement she'd always dreamed of.

"I was able to feel more in control of my finances," Gail said. "I'm more confident and way less stressed about money. It's amazing how much peace of mind you get when you have a financial guide."

If you're a business owner drowning in expenses despite your success, you can get the same guidance that helped Gail eliminate debt and build her retirement foundation.