Becoming a new mom is an exciting and challenging time in your life. Along with all the joys of motherhood, you must also consider new financial responsibilities.

Financial planning for new moms involves many considerations, from budgeting for diapers and baby food to planning for their future education and other unexpected costs.

Let's look at some important financial planning tips you should remember as a new mom.

Now that you have a new member in the family, it's important to review your budget and make any necessary adjustments. Consider any changes in income, expenses, and savings goals that may arise with a new baby.

Doing Well is here to provide personalized support and guidance that aligns with the dynamics of your evolving family.

Create a realistic budget that accounts for all your current and future expenses. This will help you stay on track with your finances and avoid overspending.

Here are some practical tips:

Certain employers and state initiatives provide maternity and/or paternity leave benefits. Here’s a quick guide:

Parents, on average, spend $233,610 to raise a child until they turn 18. This figure excludes the annual costs of college.

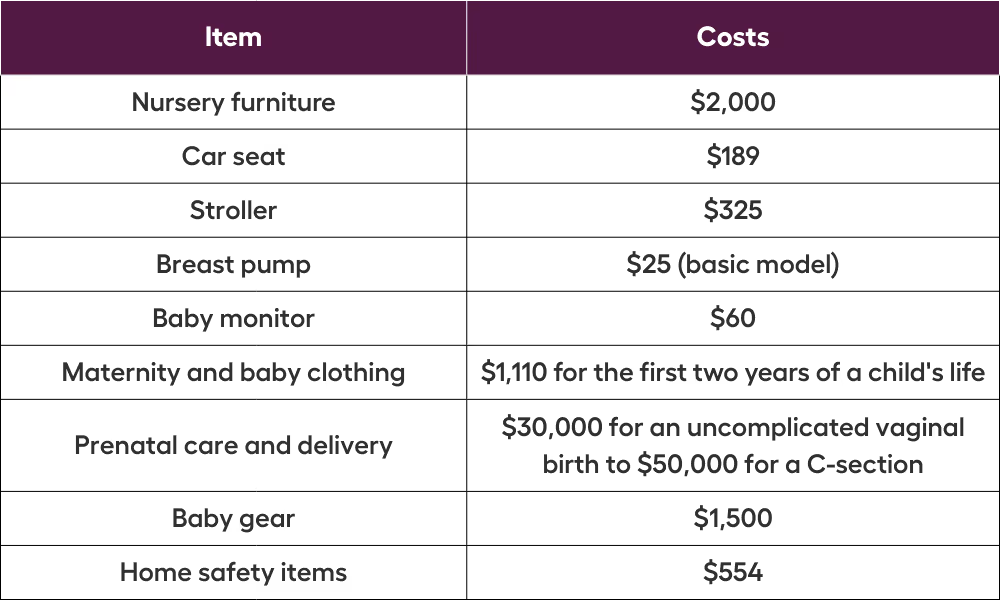

Understanding the costs of raising a child is important, including both one-time and recurring expenses. Here are some examples and the estimated costs of each:

Having an emergency fund is crucial for new moms. This financial cushion can help cover unexpected expenses like medical emergencies or job loss. You should save at least three to six months' worth of expenses in your emergency fund.

If you don't have an emergency fund, start building it by setting aside a small portion of your monthly income. If you already have one, consider increasing the amount you contribute each month to account for any additional expenses that may arise with a new baby.

As a new mom, reviewing and updating your insurance policies is important. Consider purchasing or increasing coverage for both life and disability insurance.

As a first-time mom, ensuring your child's welfare is crucial to securing their financial future. One way to do this is by reviewing and updating your beneficiaries on all your accounts, including life insurance, retirement plans, and bank accounts.

Make sure your child is listed as a beneficiary on these accounts. You may also consider setting up a trust for your child's inheritance. Consult an estate planning attorney or financial advisor for the best options for you and your family.

A power of attorney (POA) is a powerful tool that allows you to appoint someone you trust to manage your affairs if you cannot do so yourself.

This could be due to illness, disability, or other unforeseen circumstances.

It ensures that your financial foundation remains intact and your family's needs are met even during unexpected events.

Along with creating a POA, reviewing and updating your estate planning documents is important. It includes your will, trust, and any other legal documentation outlining the distribution of your assets.

The POA also outlines who will care for your child/children if something happens to you. This will ensure that they're cared for by someone you trust.

Additionally, the rules surrounding minors inheriting money or assets can be complex, making it important to consult an estate planning attorney or financial advisor. They can help ensure everything is in order and tailored to your needs and wishes.

Having a child can potentially provide you with some tax breaks and benefits. Some common ones include:

College may seem far away, but it's never too early to start considering your child's education. The earlier you start saving, the more time your money will have to grow.

Some options for educational savings include 529 plans, Coverdell Education Savings Accounts (ESAs), and custodial accounts (UGMA/UTMA). Consider discussing these options with a financial advisor to determine which fits your needs and goals best.

As a new mom, your natural instinct is to use all your resources to secure your baby's future. However, it's equally important to save for your retirement.

There are multiple avenues for your child to finance their college education—scholarships, student loans, and grants—but your retirement savings don't enjoy the same flexibility.

Consider these actionable steps:

Whether you plan to return to work after having a baby or not, making a career plan is important.

If you're returning to work, consider these steps:

If you're not returning to work, consider these steps:

New moms face the challenge of adjusting their financial plans to accommodate the needs of their growing families. Doing Well is here to support you in this transition by providing you with the tools and knowledge necessary to:

Remember, managing your finances isn't just about daily expenses; it's about ensuring a prosperous future for you and your child. With Doing Well as your partner, confidently handle personal finance with clarity, making decisions that benefit your family now and in the future.

Book your free consultation here.